.png)

A major tax reform has been adopted in Luxembourg and will come into force on 1 January 2028. What impact will it have on households?

Towards greater tax equality

In 2023, the intention to reform taxation was included in the government programme. This reform was adopted in 2026 and will come into force on 1 January 2028. It will apply for the first time to income from the 2028 tax year (to be filed in 2029).

The main objective is to introduce a single tax class and put an end to the current three-class system.

Currently, Luxembourg operates with three tax classes:

- Class 1, which includes single or divorced individuals without dependent children.

- Class 1A, which applies to single parents, pensioners or certain specific situations. It is the most advantageous, particularly aimed at reducing the tax burden for single-parent households.

- Class 2, which applies to married or civil partnership couples with joint taxation (income splitting). This allows access to lower tax brackets, especially if one partner earns significantly less than the other.

From 2028, these three classes will be replaced by a single class called Class U.

This new system is based on individual taxation, meaning each taxpayer will be taxed independently, regardless of marital status.

The new tax scale is largely based on the current Class 1A and introduces several major changes:

- An exemption threshold raised to €26,650, compared with around €13,230 today.

- A simplified tax scale with fewer classes.

- A more neutral tax system with regard to marriage or civil partnerships.

This reform, therefore, marks the end of taking marital status into account when calculating income tax, a principle that has been in place since 1842.

If you wish to learn how to complete your 2026 tax return, you can find all the useful information in our guide.

The reasons behind the government’s decision

This reform is estimated to cost the Luxembourg government between 850 million and 1 billion euros a year.

Despite this high cost, it aims to establish a fairer tax system that is better suited to today’s society.

Indeed, the current system is still largely based on an outdated model (from 1960), in which only one partner in a household worked. Today, circumstances have changed:

- Most households now have two incomes (the employment rate of the second partner is now 67%).

- The number of single individuals is increasing.

- Family and relationship structures have diversified.

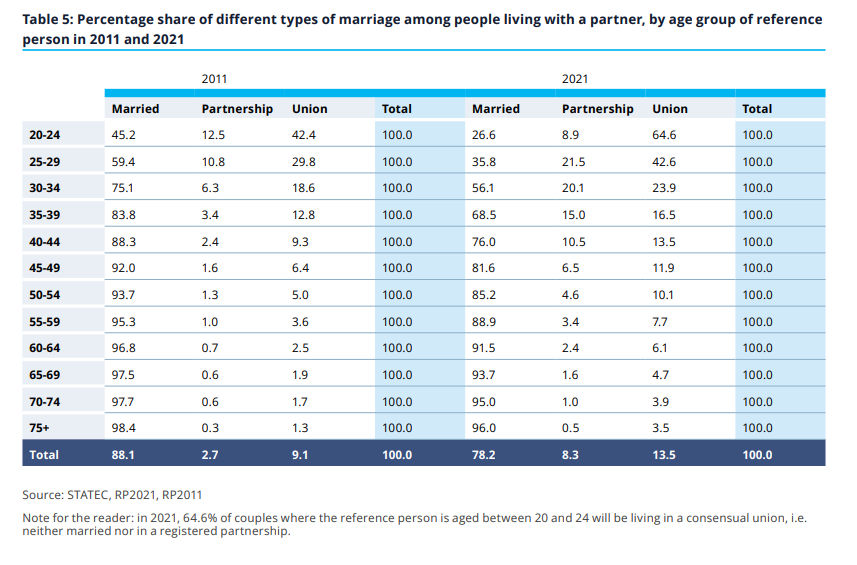

A study by STATEC shows that over 10 years (2011-2021), the proportion of married couples has significantly decreased, particularly among younger people. Meanwhile, the number of civil partnerships has increased. With the end of tax advantages, these figures could decline again from 2028.

Graph from STATEC about the marital status of households in Luxembourg.

The impact of these changes on the purchasing power of Luxembourg residents

The new tax system will have different effects depending on individual circumstances.

In general:

- Taxpayers currently in classes 1 and 1A will mostly benefit.

- Around 85% of those in Class 2 are also expected to see a tax reduction.

Single individuals and couples with similar incomes are likely to be the main beneficiaries of the reform.

However, some couples with significant income disparities may be disadvantaged, as they will no longer benefit from income splitting.

To avoid sudden financial losses, a 25-year transition period has been introduced:

- Couples already married or in a civil partnership before 2028 will be able to keep the current system (Class 2).

- They will also have the option to switch to the new system if it is more advantageous.

- Once the choice is made, it cannot be reversed.

This reform aims to create a fairer and more balanced tax system for everyone.

Find more articles about taxation in Luxembourg on our blog.